How Do Households with Low and Moderate Incomes Build Wealth, and How Can Practitioners Improve These Pathways?

Editor’s Note: This post was originally published by the Urban Institute on May 7, 2026. It is a guest cross-post which features JUST’s social capital lending model and republished here with permission. The full report and original analysis were authored by Brett Theodos and Brady Meixell and can be read here.

READ TIME: 6 mins

Building even a small amount of wealth can reduce a household’s risk of economic hardship, create stability, and serve as a springboard to economic mobility. But many American households today feel that building wealth is out of their reach, particularly in the face of the broader affordability crisis.

This raises two questions:

How much wealth do households with low and moderate incomes (LMI) have?

What pathways could help these households build greater wealth?

To identify potential pathways, we explore wealth and wealth building among working households—those whose primary earner is in the labor force and in their prime working years (ages 25 to 65)—with LMI, defined as income below the national median of $83,730.

We find that despite substantial disparities in wealth among working households with LMI, these households use business equity, home equity, and retirement savings to create wealth. Understanding these pathways can help practitioners and policymakers design better tools, supports, and policies to help more families build assets over time and achieve long-term financial stability.

How much wealth do working households with LMI hold?

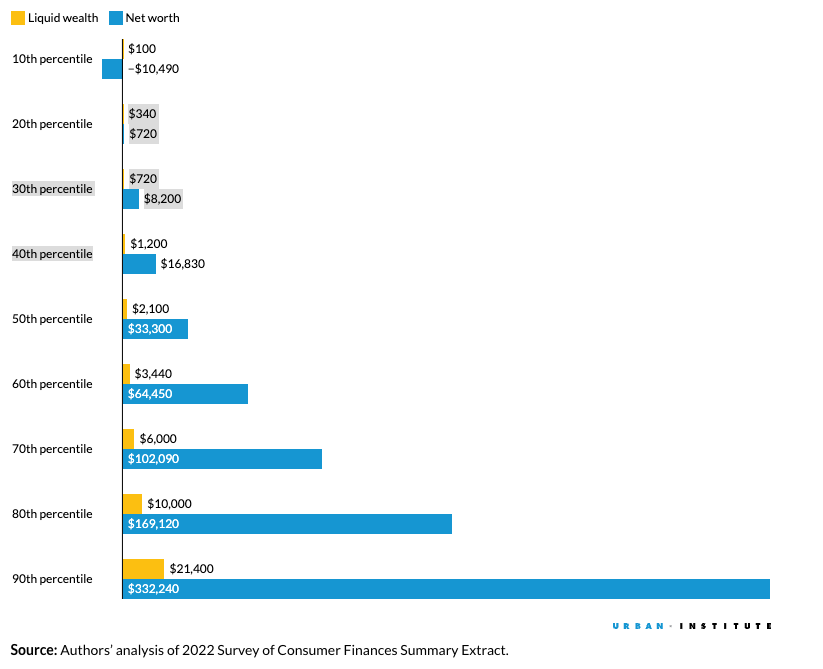

Working households with LMI have a median net worth of $33,300. Their average net worth is $144,062, implying there’s also a concentration of wealth among this group. Among working households with LMI, those at the 90th percentile hold over $330,000 in net worth and over $21,000 in liquid assets.

Most Working Households with LMI Don’t Have the Liquid Savings to Cover a Financial Emergency

Liquid wealth and net worth among working households with LMI by percentile

Source: Authors’ analysis of 2022 Survey of Consumer Finances Summary Extract.

Notes: LMI = low and moderate income. Working households with LMI are defined as those with primary earner ages 25-65 and in the labor force, and household income below the national median of $83,730 (in 2024 inflation-adjusted dollars). Liquid accounts do not include retirement accounts.

By comparison, those at the bottom 10th percentile have –$10,490 in net worth (meaning their debt outweighs their assets) and only $100 in liquid assets. Nearly half of LMI working households don’t have liquid savings to cover the average cost of a financial emergency, such as car or home repair, which is around $1,700.

Still, research shows families with even modest nonretirement savings are less likely to be evicted or miss housing or utility payments.

There’s also evidence of meaningful wealth building as well. Having low or moderate incomes doesn’t necessarily imply that a household has low liquid savings or net worth. For example, the 70th percentile has over $100,000 in net worth.

How do working households with LMI build wealth?

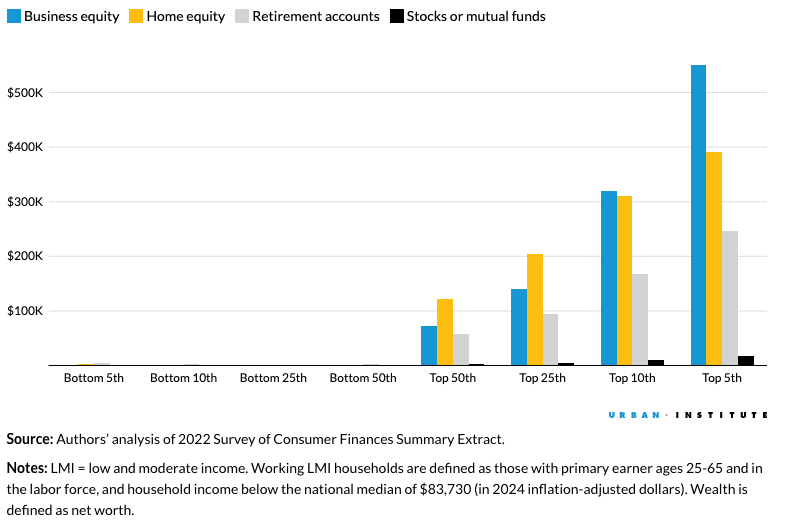

Among working households with LMI, we find that business ownership most substantially contributes to wealth. The top half of these households held, on average, more than $73,000 in business equity.

Still, only 10 percent of working households with LMI are business owners, and businesses can have different success trajectories.

Home equity and retirement are also substantial drivers of wealth for working households with LMI, with both being more prevalent and a larger percentage of total wealth than business ownership among working households at the bottom half of the wealth distribution.

Sources of Wealth Building Among Working LMI Households

Average amount working LMI households have of a given asset, by wealth distribution level

Source: Authors’ analysis of 2022 Survey of Consumer Finances Summary Extract

Notes: LMI = low and moderate income. Working LMI households are defined as those with primary earner ages 25-65 and in the labor force, and household income below the national median of $83,730 (in 2024 inflation-adjusted dollars). Wealth is defined as net worth.

Retirement equity starts to rise significantly beginning at the top 50th percentile of working households with LMI. Though retirement equity is not liquid in the traditional sense, new provisions in the 2022 SECURE 2.0 Act allow households with retirement accounts to withdraw up to $1,000 penalty free for emergencies (PDF).

How can the community development finance ecosystem expand access to wealth-building pathways for working households with LMI?

Though households with LMI have found pathways to build wealth, differences within this group remain stark. By strengthening these pathways, members of the community development finance ecosystem can help more working families create wealth and improve their financial well-being.

Owning a business is an underappreciated pathway for wealth building for households with LMI. Traditional loan underwriting requirements like credit scores, collateral, and cash flow analysis can impede starting a business for communities and borrowers with LMI.

To lessen these barriers to entry, JUST, a Texas-based nonprofit community development financial institution, leverages social capital to integrate business loans, coaching, and peer support.

Community wealth-building models are another approach. These allow individuals to build their personal wealth by participating in commercial transactions that generate returns; pool community resources to lower the cost of homeownership; or deploy capital to provide affordable spaces to small businesses.

The asset building, entrepreneurship support, and community development finance fields can also help address the gaps in wealth-building pathways by designing tools, products, and approaches that both help build protective liquid savings for financial emergencies and provide footholds to building ownership in more sizable assets.

Important questions remain. Can liquid savings function as a catalyst for future wealth building? Does reaching certain savings milestones reliably help advance homeownership, business investment, or retirement security among LMI households? What financial products can help households hold onto their new assets and not lose ground as they progress? Are these households using other new pathways to build wealth?

To meaningfully drive wealth creation and improve financial well-being for all households, community asset builders, entrepreneurship supporters, and community development financiers need to not only provide capital solutions but also explore new models that meet the holistic savings, debt, and advisory needs of households, business owners, and communities with low and moderate incomes.